The idea of paying a $100 annual fee for a credit card can be off-putting and prevent many people from ever starting the Game of Miles. But if you’ve read my other posts and have made it to this one, you hopefully see that the large sign up bonuses almost always make the annual fee worth paying for the first year. But what about after the first year? Should you continue paying the annual fee or should you downgrade or cancel it? And what about the premium credit cards that have annual fees of several hundred dollars?

The choice of whether or not to pay an annual fee comes down to your spending habits and how much you value the perks offered by the card. Remember, you win the Game of Miles by earning free travel for normal, everyday spend. If a credit card offer perks and credits that are nice to have but not something you would normally pay for, you probably shouldn’t be paying the annual fee after the first year.

In this post, I’m going to do some mini reviews of cards along with comparisons of some low annual fee cards to their more expensive premium versions. I’ll be ignoring sign up bonuses so you can make judgements on the value of the cards themselves. I’ll also only focus on what I consider are the most useful and commonly used perks.

Note: never cancel or downgrade a card right after earning the bonuses. Many issuers have language in their terms that warn you of losing your points by misusing their reward program. They obviously don’t like it if you sign up their card, get the bonus, and then cancel it. You already paid the annual fee for the first year, so keep it open for that duration at minimum. When the anniversary begins approaching, look at how much you value the perks and determine if the fee is worth paying for another year. I have never had a bonus “clawed back” for downgrading or cancelling a card after the first year.

In a different post, I recommend either of these two cards as your first card. The Chase Sapphire Preferred has an annual fee (AF) of $95 while the Chase Sapphire Reserve has an AF of $550.

Both cards offer a complimentary DashPass membership so this perk won’t be a deciding factor when choosing between the two cards. However, the subscription normally costs $9.99 a month and makes justifying the AF of the Preferred a no-brainer if you are already a DashPass subscriber.

The Preferred offers $50 in statement credits each account anniversary year for hotel stays purchased through Chase’s travel portal.

The Reserve offers a $300 annual travel credit. This travel does not have to be booked through Chase’s portal and includes things such as Uber and taxi rides.

You also get luxury travel benefits with the Reserve. You receive Priority Pass Select membership that gives you access to over 1,300 airport lounges in over 500 cities worldwide. You’ll also get one statement credit of up to $100 every four years to reimburse you for TSA Precheck or Global Entry.

The last benefit that I really like from the Reserve is access to special benefits when booking from The Luxury Hotel & Resorts (LHR) Collection. This is a collection of more than 1,000 properties worldwide. The benefits often include daily breakfast for two, an onsite dining credit of $100, complimentary room upgrades when available, and early check in and late check out.

The Preferred gives you a 25% bonus to travel booked with UR points through their travel portal while the Reserve offers a 50% bonus. This equates to 1.25x and 1.5x the cash value of the points respectively. I’ll ignore both of these perks since you can almost always get a better deal than 1.25x or 1.5x the cash redemption rate if you transfer the points to one of Chase’s travel partners. Both cards allow you to transfer UR points at a 1:1 rate to the same 11 airlines and 3 hotel chains.

I’ll also ignore the bonus points you get for different categories of spend in this comparison to keep things simple. These bonus point multipliers won’t be enough to be a deciding factor since you will be switching your spending to a different card once you hit the spend requirement for the sign up offer.

So which card should you get? Many will immediately scoff at the idea of paying $550 per year for a credit card, but lets take a closer look at how much more you are really spending for the Reserve than you are for the Preferred.

If you would normally pay for a single night hotel stay per year, then the AF of the Preferred is effectively only $45 because of the $50 hotel credit. If you normally spend $300 on travel each year, then the AF on the Reserve is effectively only $250.

So you need to come up with the $205 difference between the cards to justify getting the Reserve. Being able to justify this $205 depends on how you like to travel.

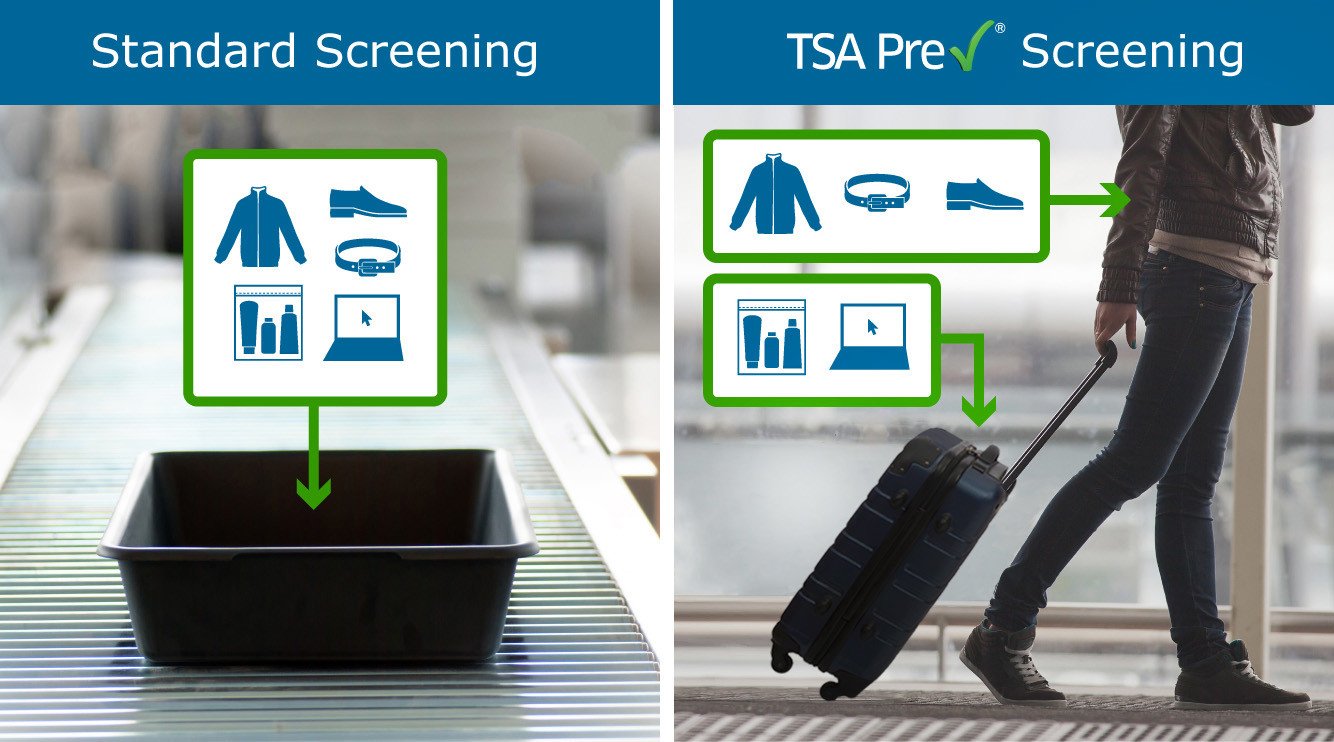

I highly recommend TSA Precheck. Hate having to get to the airport two hours early in case there is a long line at the security checkpoint? With TSA Precheck, you have your own security line that bypasses other travelers, and you won’t have to remove your shoes, laptops, or liquids when going through the security checkpoint. You can still get to the airport two hours early if it gives you peace of mind, you’ll just have more time to relax in the lounge before your flight!

This perk will save you $85. However, that gets you 5 years of TSA Precheck whether you keep the card or not so you won’t have that added value after the first year. I personally think TSA Precheck is well worth the $85 cost for 5 years of enrollment. You will too. After reimbursement for TSA Precheck enrollment, you only need to justify $120 for the Reserve to be your choice.

Another perk offered by the Reserve that I highly value is Priority Pass membership. If you want to travel in comfort, you are going to want airport lounge access. I remember I was blown away the first time I walked into an airport lounge and couldn’t believe that I had never known about them. Each lounge offers its own benefits, but nearly all offer complimentary cocktails, snacks, and far more comfort and privacy than the normal sections of the airport you are used to. Some lounges even offer full buffets and bars where you can poor your own drinks.

If you want to travel in comfort, you are going to want airport lounge access.

Each individual visit would cost you a $27 entry fee without membership. That’s typically less than what I would spend at an airport bar on a meal, drink or two, and tip. If you travel multiple times a year to any of the many airports have that have Priority Pass lounges, I would say this perk is well worth $120.

I think the elite benefits you get by booking through the LHR collection are amazing. These benefits apply even for stays of a single night. And just because the collection is labeled as Luxury does not mean all of the properties will break the bank. You can often find single night stays in the collection where room rate will nearly be covered by the breakfast credit plus the $100 on site dining credit.

If you travel frequently and value TSA Precheck and airport lounge access (which you will), the Sapphire Reserve is not a bad deal for a $550 AF, at least not for the first year. If you stay at properties in the LHR Collection one or more times a year, it’s a fantastic deal.

So do I recommend it over the Preferred? No, I do not. The reason is simple. You can get many of the same perks from other cards that offer far more overall value.

There are many $100 AF cards that will reimburse you for your TSA Precheck application. You can get the same LHR Collection benefits from Chase’s $95 United Explorer Card. There’s also a different premium card offering Priority Pass membership that I highly recommend. I’ll discuss it in the next section.

The Reserve is a great choice for those who want luxury travel benefits right out of the gate, but the Chase Sapphire Preferred is going to be the best first choice for most people starting the Game of MiIes who don’t mind waiting a little while to get the same benefits on other cards.

The Venture has an AF of $95, and the Venture X has an AF of $395.

Both cards pay for your TSA PreCheck or Global Entry application. Both cards allow you to transfer your miles to Capital One’s 14 airline and 3 hotel partners. They both earn an excellent 2x miles on all purchases.

The Venture gives you two free lounge visits per year. This includes the large network of Priority Pass lounges as well as the more limited network of Capital One’s own lounges.

The Venture is not worth the $95 AF, in my opinion. If you are playing this game right, you will have TSA PreCheck and lounge access through other cards. The 2x transferrable miles earning on all purchases is excellent, but that alone is not worth the fee. Get the sign up bonus, and then downgrade or cancel it after the first year.

As I stated in a previous post, I consider the Venture X to be the best credit card currently on the market. It is the main reason that I can’t recommend the Sapphire Reserve. This card offers incredible value and, to be honest, should have an AF much higher than $395.

With the Venture X, you get unlimited lounge visits and 2 complimentary guest passes per visit.

The Venture X gives you an annual $300 credit for travel booked through their travel portal. The portal offers price matching and earns 5x miles on airfare and an amazing 10x miles on hotels and rental cars booked through it when paying with the Venture X. You also get 10,000 bonus miles every year beginning with your first anniversary. That is worth a minimum of $100 if redeemed for cash back (which you won’t be doing since you can get much better value when transferring to a travel partner).

And right there you have it. Those two perks alone mean that you are coming out ahead at least $5 a year. At that point, the TSA Precheck/Global Entry credit and Priority Pass Membership are just added benefits. And with the unlimited 2x earning on all purchases, this card will never leave your wallet. If you normally spend $300 a year combined on hotels, airfare, and rental cars, there is absolutely no reason not to have the Venture X.

Co-branded hotel credit cards won’t be for everyone especially if you aren’t loyal to one single hotel brand. I still want to compare these two cards to give you an idea if either could be right for you.

The Surpass has an AF of $95, and the Aspire has an AF of $450.

The Surpass is going to give you 10 complimentary visits to Priority Pass lounges per year along with complimentary Hilton Gold Status.

If you don’t have access to Priority Pass lounges through a different card, the 10 complimentary visits are a nice perk to have on a low AF card and more than enough visits per year for a lot of travelers.

Hilton Honors Gold status gives you a number of perks when staying at Hilton properties including space-available room upgrades, daily food and beverage credits, and fifth night free on award stays. The fifth night free on award stays is an excellent perk, and the points you get from the sign up bonus will give you a jump start to be able to take advantage of this perk for great value.

The Aspire offers many perks that more than make up for the $450 AF for many travelers. It offers an annual $250 credit towards incidental airline fees. You choose one airline each year from AMEX’s selection of airlines where this credit can be applied. The incidental fees that can be credited include fees for checked baggage, in-flight refreshments, and seat change fees. Not everyone can max out this credit on a single airline in a year, but I find it easy to between in-flight refreshments and seat assignment fees.

The Aspire also offers a $250 annual Hilton Resort credit for eligible purchases at participating Hilton Resorts. Eligible purchases include the room rates themselves.

After one year with the card, you get a free night certificate each year on your card anniversary. In another post, I give a few examples of how I’ve used this certificate. I easily get more than $400 in value from these certificates every year.

You also get Priority Pass membership as well as complimentary Hilton Honors Diamond status. Diamond status is the highest status you can achieve with Hilton. Diamond status is a tremendous perk if you stay at Hilton properties a few times a year. I have found that Hilton is very generous with upgrading Diamond members even on stays booked only with points. I’ve been upgraded to both Presidential and Skyline suites which were upgrades worth several hundred dollars per night.

A premium credit card with a large annual fee is often easier to justify paying for than a credit card with a low annual fee.

The Aspire is an incredible card and a great example of how premium credit cards often offer so much more value than what you are paying in an annual fee. A premium credit card with a large annual fee is often easier to justify paying for than a credit card with a low annual fee. If you can max out the airline and resort credits through normal, everyday spend, you are being paid $50 per year just to have this card. Priority Pass membership, the annual free night certificate, and the impressive complimentary Diamond status are just added bonuses.

The last card I’m going to cover in this post is the American Express Platinum Card. The $695 AF of this card is one of the highest in the game. But if you’ve made it to this point in this post, hopefully you are asking what it has to offer to justify that cost instead of just dismissing it based on the cost of the AF alone.

The fee was raised from $550 to $695 in 2021. I have this card and was only charged the $550 AF on my most recent renewal even after it was raised. Besides helping you determine if this card is right for you, this section will also help me to determine if I can justify paying the increased $695 AF when it comes time for me to renew again.

This card offers a ton of perks (it should at its price point), but you likely won’t find all of them useful. The featured perks are a $200 hotel credit, $200 airline incidental fee credit, $155 Walmart+ credit, $240 digital entertainment credit, $200 in Uber Cash, $300 Equinox credit, $300 SoulCycle at-home bike credit, $189 CLEAR credit, $100 Saks credit, and access to the American Express Global Lounge Collection. All of the credits are given annually.

The $200 hotel credit can be used on prepaid Fine Hotels + Resorts or The Hotel Collection bookings. FHR bookings only require a one night minimum booking while THC require a minimum of 2 nights. FHR bookings include some great perks such complimentary room upgrades when available, early check in when available, guaranteed 4pm late check out, and daily breakfast for two. Many of the FHR properties also include an additional $100 property credit. I don’t find it difficult to max out this credit each year. I can often find a one or two night FHR stay at a destination I’m traveling to that more than pays for itself between the $200 booking credit and $100 property credit.

The $200 airline incidental fee credit works the same as the Hilton Aspire card and is an excellent perk if you can max it out.

The Walmart+ credit is given as a $12.95 statement credit each month to cover the cost of membership. I don’t value this credit at all since I rarely shop online at Walmart and would never pay for Walmart+ membership. However, if you already subscribe to Walmart+, this credit will be great for you.

The digital entertainment credit is credited on up to $20 in monthly charges to any combination of The Disney Bundle, Disney+, Hulu, ESPN+, Peacock, The New York Times, Audible, and Sirius XM. This is a pretty solid combination of services, but it would be unlikely that I would get enough use out of them to justify paying $240 per year. For myself, I will only value this perk as worth $60 based on my normal spending habits. I wouldn’t have a problem paying $60 per year for a combination of these services. I’m sure there are many people that are already paying $240 per year for these services so they will value this perk higher than I do.

The $200 Uber Cash is credited $15 per month with December getting a $25 credit. The credit has to be used each month and cannot be carried over to the next. It’s good for both Uber rides and Uber Eats. I spend a minimum of $15 a month between Uber and Uber Eats so this perk is great for me.

You get Hilton Honors Gold and Marriott Bonvoy Gold Elite status with the Platinum card. These don’t factor into my decision to keep the card since I have Hilton Diamond status with my Aspire card and consider Marriott Gold status to be near worthless. You might value these statuses differently, though.

I don’t use either the Equinox or SoulCycle credit so I value them at $0. However, some of you may find them valuable.

The Saks credit is given as $50 twice a year. I don’t shop at Saks, but I do sometimes use this credit to buy cheap gifts from them. Since this is not normal spend for me, I value this perk at $0.

CLEAR membership pairs great with TSA PreCheck. CLEAR uses biometrics to verify your identity allowing you bypass the ID check at the airport. At the airport, you walk up to a CLEAR attendant who will scan your biometrics. From there, they will escort you directly to the TSA agent checking IDs and boarding passes. You flash your boarding pass and move on to the security screening. There is no need to show the agent your ID or passport.

CLEAR is just a quicker way of having your identity verified. If you have TSA PreCheck, it won’t save you much time going through security since the TSA PreCheck line is usually pretty short. CLEAR does not give you an expedited screening process like TSA PreCheck does.

Paired together, CLEAR and TSA PreCheck can usually get you through security screening in less than 5 minutes. However, TSA PreCheck can get close to that on its own.

I wouldn’t pay money out of pocket to enroll in CLEAR so I value this perk at $0, although I really do enjoy having it and would definitely miss it if I cancel my Platinum card.

The last perk that I find valuable is access to the AMEX Global Lounge Collection. This includes AMEX Centurion lounges, Delta Sky Club lounges, Priority Pass lounges, along with some others. The Centurion lounges are often far superior to the Priority Pass lounges but are not as easy to find.

So will I be keeping this card if my AF is raised to $695 this year?

I have no problem maxing out the hotel and airline credits with the amount of money I normally spend on travel each year. I spend at least $15 a month on Uber/Uber Eats with or without the card. The digital entertainment credit is pretty solid, but I would probably only pay for some of the streaming services a few months out of the year. I will only value this perk as worth $60 based on my normal spending habits.

The $200 hotel credit, the $200 airline credit, the $200 Uber Cash, and the $60 that I value the digital entertainment credit at would cost me $660 a year in normal, everyday spend leaving $35 in value needed to justify the annual fee.

I would gladly pay $35 per year for access to the American Express Centurion lounges especially since there is one at my home airport. Even though I highly value Priority Pass membership, Centurion lounges are on a different level. And because the cards needed to access them come at such a high price, less people can get in resulting in less overcrowding. Luckily for us, not everyone knows that this card is well worth the annual fee.

So, yes, I will be keeping this card. The $695 AF is steep, but for me it makes perfect sense. It may also make sense for you depending on how you value the perks. Keep in mind that there are many other perks to this card that I didn’t even mention. They are just bonuses if you can justify the AF based on your normal, everyday spending habits.

Don’t let a credit card’s annual fee prevent you from playing the Game of Miles. And consider the premium credit cards with high annual fees if you never have before. A card’s perks will often reimburse you for travel and services that you are already spending money on. If that is the case, you are just prepaying for your normal, everyday spend when you pay the fee.

If you found the information here helpful and decide to apply for any of the cards mentioned, please consider signing up through my referral links (if available) on the home page.

Disclosure: The information provided on my blog is for entertainment and educational purposes only and should not be considered financial or tax advice. While I try to provide accurate information, readers should verify the accuracy and up-to-date status of any information on the blog and to do their own research before making any decisions. I may receive a point bonus or reward from the company when a reader signs up for a product or service through one of my referral links, but this is not part of any special arrangement with the companies mentioned. I do not receive any other compensation or have any other arrangement to be compensated from any company mentioned in the blog. All opinions are my own. I am not affiliated with any of the companies mentioned on this blog. The views and opinions expressed on this blog are solely mine and do not represent the views or opinions of any providers. Thank you for your support!

Your message was successfully sent. Thanks for reading my blog!